Click the above image for a larger image

- Sign up to our Newsletter here.

- Need assistance with an emoney or payments authorisation or an account information service provider or virtual asset services provider registration application, check out Fintech Ireland and CompliReg's handy authorisation guides at https://fintechireland.com/fintech-authorisations.html.

- Attend, exhibit and/or sponsor the upcoming Fintech Ireland Summit. Details here.

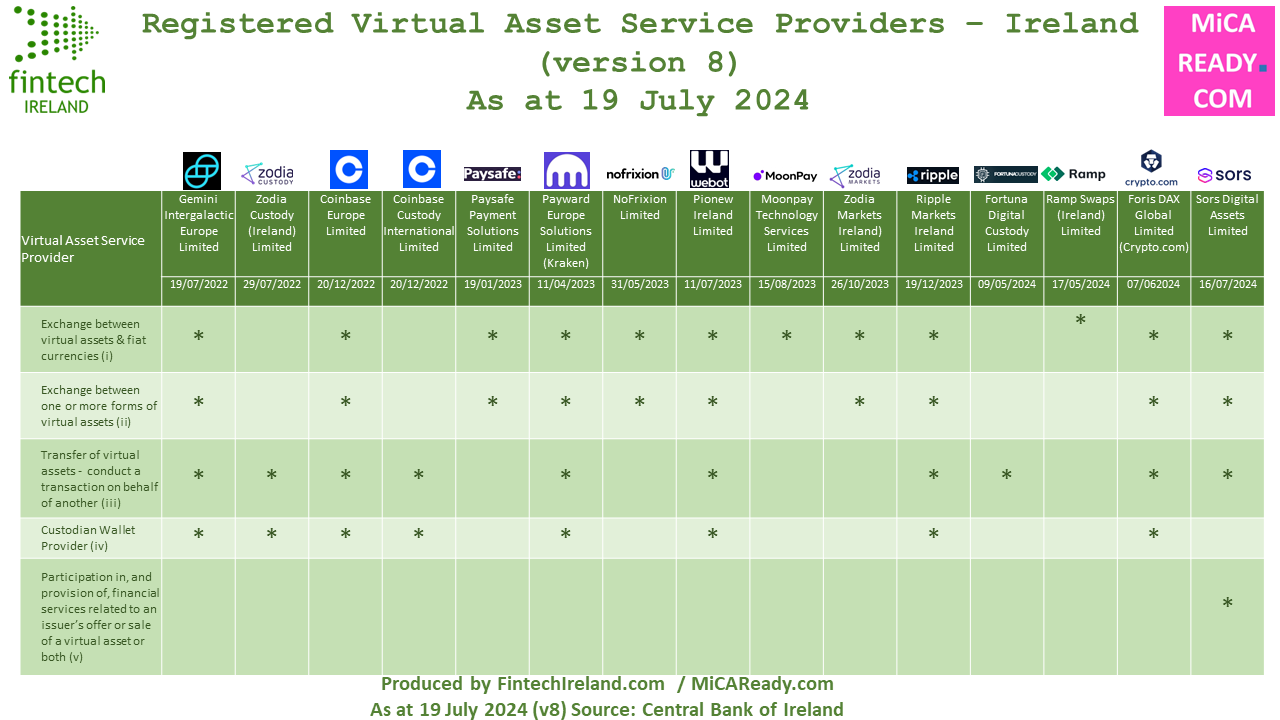

Foris DAX Global Limited (aka Crypto.com) and Sors Digital Assets Limited

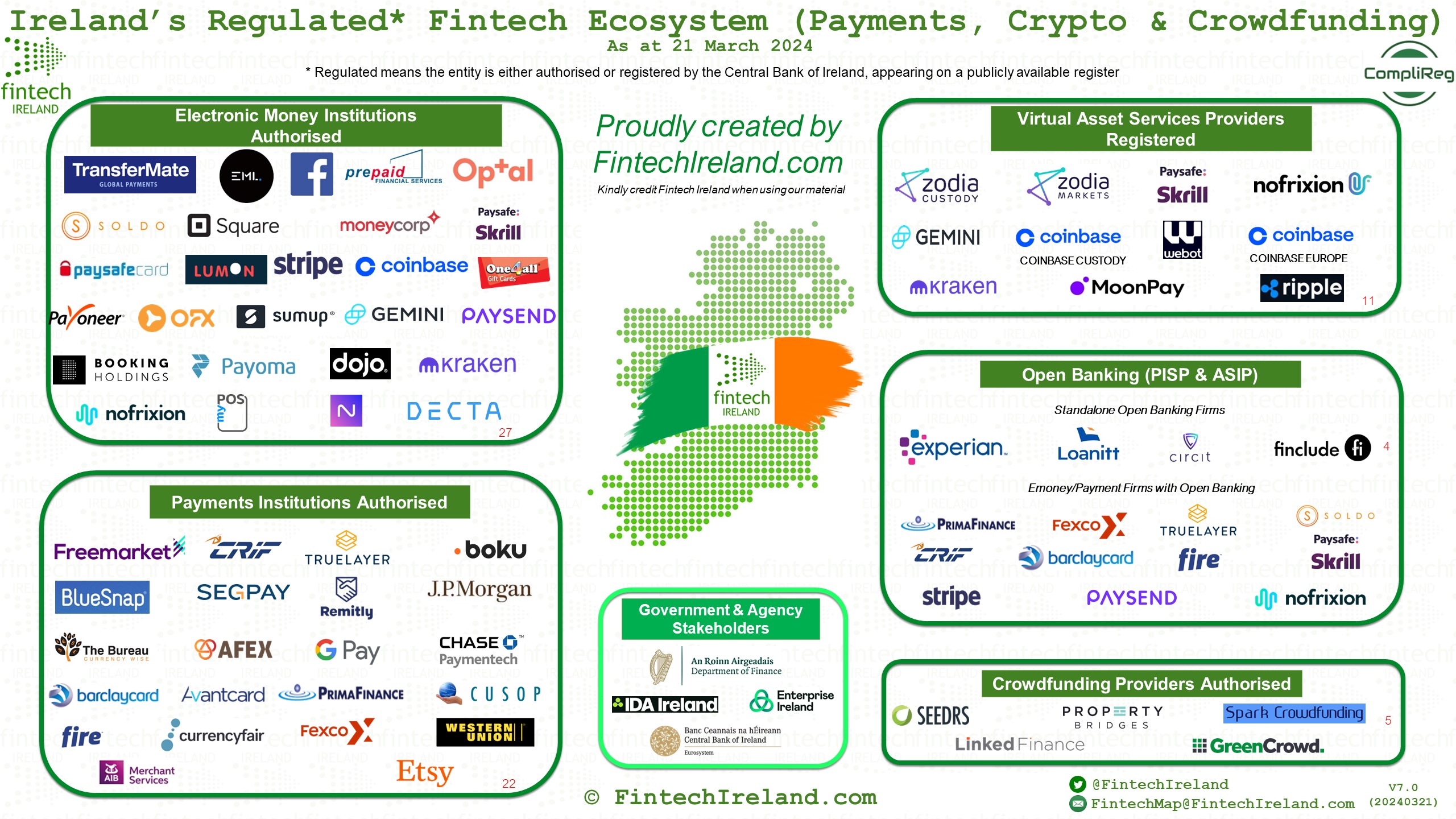

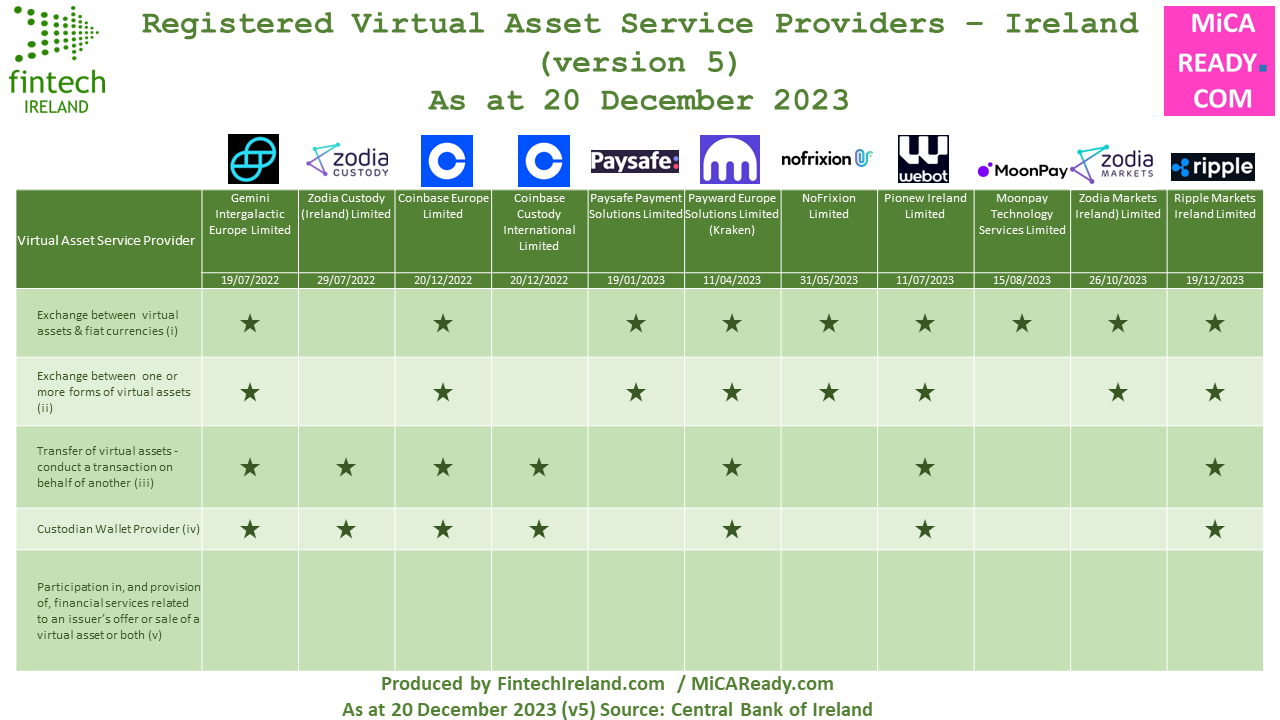

Ireland is now home to at least 75 regulated fintechs with the registrations of both Foris DAX Global Limited (aka Crypto.com) and Sors Digital Assets Limited. The two companies were registered by the Central Bank of Ireland under the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 as virtual asset service providers. To remind, VASPs are not authorised but registered to provide their services.

Linkedin Post here: https://www.linkedin.com/posts/peteroakes_cryptoasset-virtualasset-micar-activity-7219828976863641601-fNxw

Fintech Ireland is delighted to welcome both firms to the ever-growing Regulated Fintech Map (Version 11) and the VASP Map (version 8). Thanks to CompliReg and MiCA Ready which support firms in the in the #cryptoasset / #virtualasset industry.

By the way, did you know that today (19 July 2024) is the second anniversary of the very first registration of a VASP? That honour belongs to Gemini Intergalactic Europe Limited which was registered on 19 July two years ago. Happy anniversary!

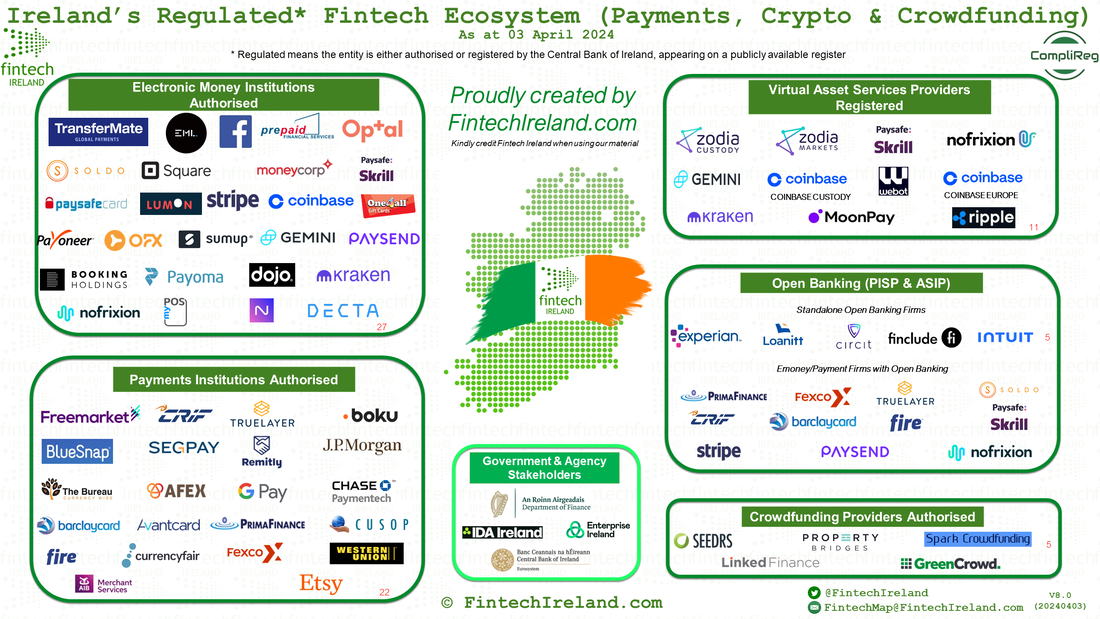

This registration of Crypto.com on 7 June 2024 and Sors Digital Assets on 16 July 2024 increases the pool of regulated fintech in Ireland to at least 75, comprised of:

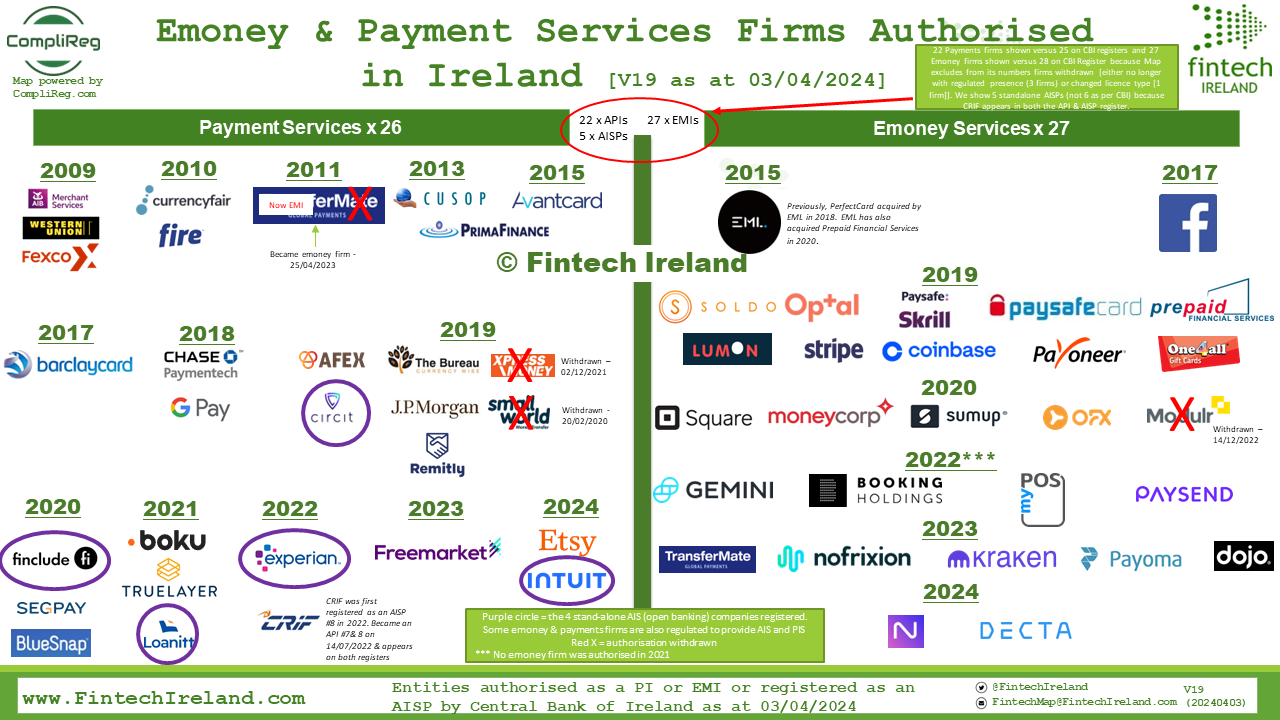

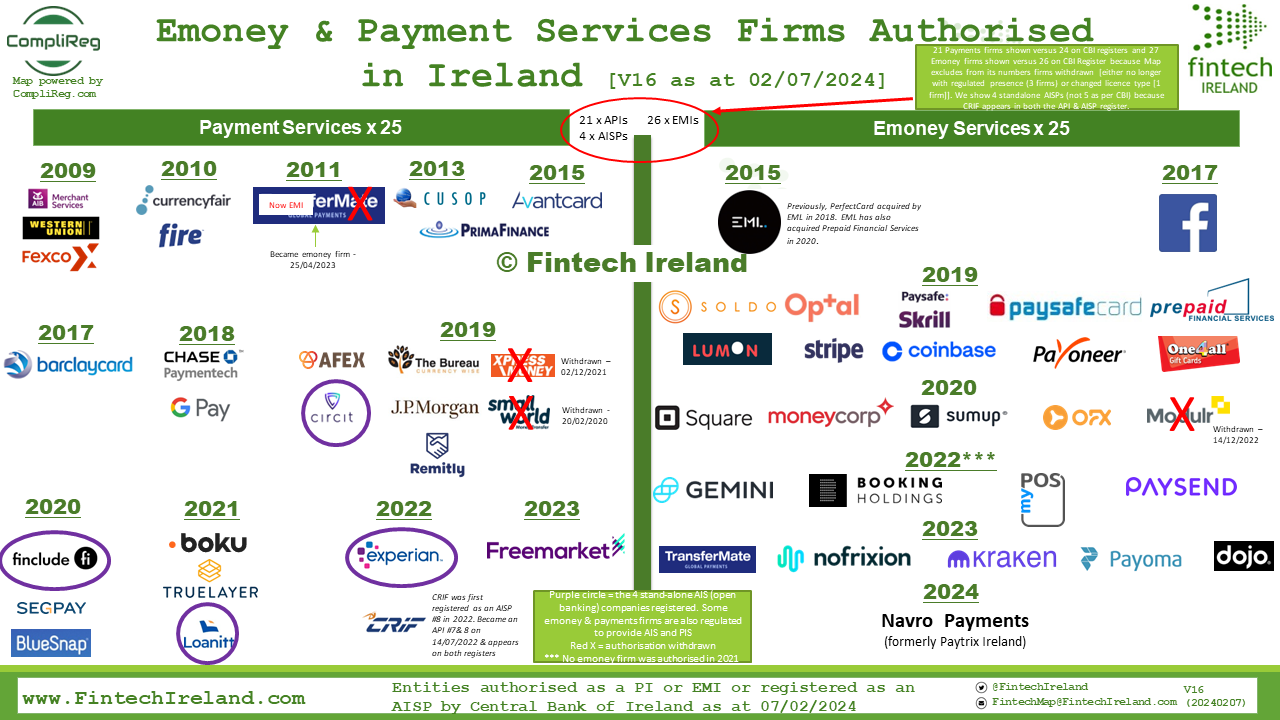

* 27 authorised electronic money institutions

* 22 payments institutions,

* 6 standalone open banking firms,

* 15 VASP, and

* 5 crowdfunding services providers.

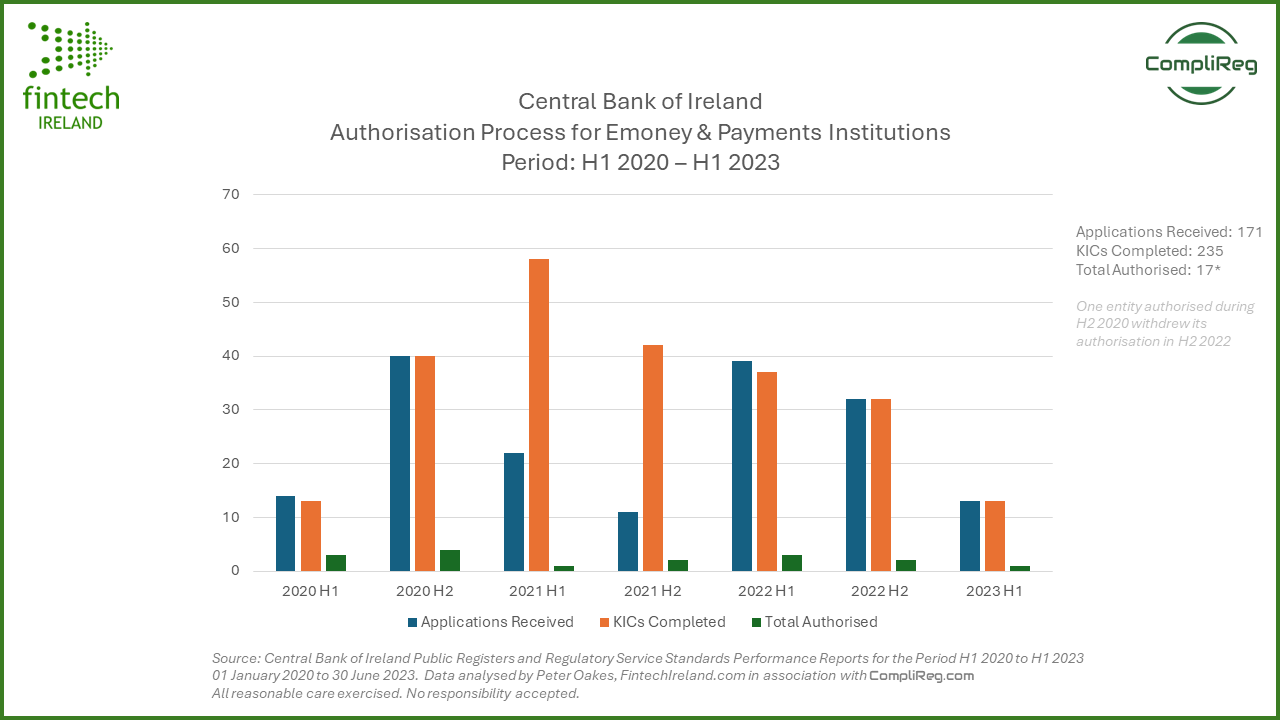

Those who read the recent Authorisation and Gatekeeping Report issued by the Central bank of Ireland might recall:

Linkedin Post here: https://www.linkedin.com/posts/peteroakes_cryptoasset-virtualasset-micar-activity-7219828976863641601-fNxw

Fintech Ireland is delighted to welcome both firms to the ever-growing Regulated Fintech Map (Version 11) and the VASP Map (version 8). Thanks to CompliReg and MiCA Ready which support firms in the in the #cryptoasset / #virtualasset industry.

By the way, did you know that today (19 July 2024) is the second anniversary of the very first registration of a VASP? That honour belongs to Gemini Intergalactic Europe Limited which was registered on 19 July two years ago. Happy anniversary!

This registration of Crypto.com on 7 June 2024 and Sors Digital Assets on 16 July 2024 increases the pool of regulated fintech in Ireland to at least 75, comprised of:

* 27 authorised electronic money institutions

* 22 payments institutions,

* 6 standalone open banking firms,

* 15 VASP, and

* 5 crowdfunding services providers.

Those who read the recent Authorisation and Gatekeeping Report issued by the Central bank of Ireland might recall:

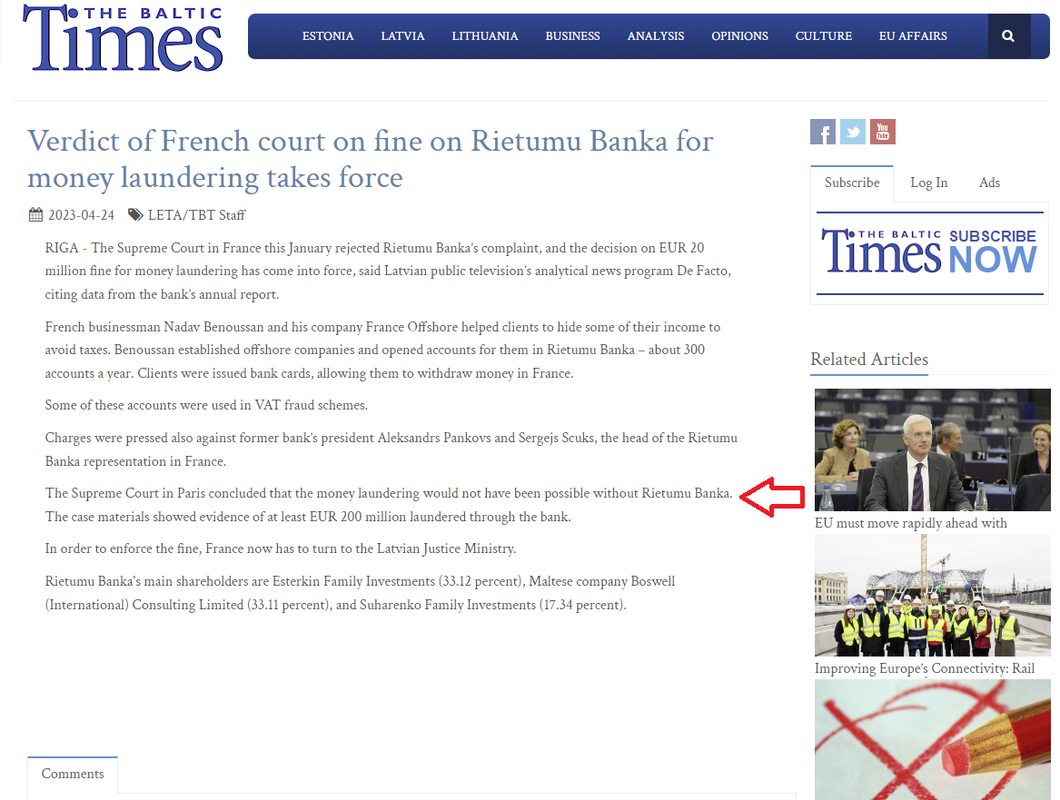

- that as at 31 December 2023 there were 14 applicants for a VASP registration in the pipeline as at that date. Obviously deduct 2, and that means if there have been no withdrawals and no new applications, we might see a further 12 firms become registered before year’s end. If that is the case the Central Bank will have its work cut out for itself dealing with potentially 27 MiCAR applications. Of course, it would be wise to assume that further companies have applied for registration since the start of this year.

- the average number of days taken to register a VASP is 530 calendar days and is largely driven by time taken by the applicants to respond to queries raised during the assessment. A significant number of firms have withdrawn from the registration process.

Click the above image for a larger image

According to Companies Registration Office Records, Sors Digital Assets is a shareholder (32.67%) in Fortuna Digital Custody Ltd which was registered as a VASP by the Central Bank of Ireland earlier this year on 9 May 2024. Sors Digital Assets is owned by Brian Elders (55%) and Stephen Browne (45%). Brian Elders is a director of both Sors Digital Assets and Fortuna Custody Ltd. Sors Digital Assets had net assets of €769K as at 31 December 2023. Stephen Browne is another director of Sors Digital Assets.

Foris DAX Global Limited is wholly owned by Foris Dax Holdings Ltd. Its directors are Mariana Dinkova Gospodinova, Rafael De Marco E Melo and Antonio Alvarez Lorenzo. Within the Crypto.com group, Mariana serves as EVP Operations & GM Europe; Rafael is co-founder and CFO; and Antonio is Group Chief Compliance Officer. Crypto.com's VASP registered operations made a small overall profit (comprehensive income) of €71.4K in the year to 31 December 2022 well down on the €3.120M profit for the previous year. The company's net assets as at 31 December 2022 were €3.2M.

We wish both Crypto.com and Sors Digital Assets the very best success for their future endeavours.

Foris DAX Global Limited is wholly owned by Foris Dax Holdings Ltd. Its directors are Mariana Dinkova Gospodinova, Rafael De Marco E Melo and Antonio Alvarez Lorenzo. Within the Crypto.com group, Mariana serves as EVP Operations & GM Europe; Rafael is co-founder and CFO; and Antonio is Group Chief Compliance Officer. Crypto.com's VASP registered operations made a small overall profit (comprehensive income) of €71.4K in the year to 31 December 2022 well down on the €3.120M profit for the previous year. The company's net assets as at 31 December 2022 were €3.2M.

We wish both Crypto.com and Sors Digital Assets the very best success for their future endeavours.

Don't forget to check out the upcoming Fintech Ireland Summit taking place on Thursday 28th November 2024 in Dublin.